January 30, 2026

New Zealand Residential Markets: Selective Re-Engagement Underway

Share

New Zealand’s easing window (325bps since July 2024) is creating a transitional phase where capital scarcity remains elevated despite improving forward economic conditions. This dislocation is favouring private credit providers able to offer certainty of funding, speed of execution and bespoke structuring. Against this backdrop, the Fund has recently deployed capital into Stage 1 of the Lakeview Te Taumata precinct in Queenstown, providing an example of selective re-engagement as the cycle turns into asset-backed projects with strong feasibilities.

Key insights:

- The seven-stage Lakeview master-planned development has secured more than NZD$150m of pre-sales for Stage 1, including a record NZD$33m penthouse transaction.

- The Queenstown-Lakes region delivered median resale gains of approximately NZD$480k in 2025 and recorded the lowest proportion of resale losses nationally, reinforcing the regional outperformance and structural demand.

- The Lakeview facility represents a repeat lending relationship with Ninety Four Feet, following the successful repayment of the NZD$160m Hotel Indigo Auckland mixed-use construction facility in 2025 and prior to this investment, the AUD$40m Open Court A-Grade office development facility in Melbourne.

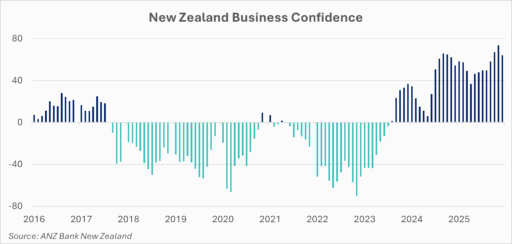

- New Zealand macro momentum is improving, with manufacturing activity, labour force participation and business sentiment all reaching multi-year highs, supporting construction activity and broader real asset demand.

- Across the Fund’s approximately $450m of New Zealand exposure spanning commercial real estate and agriculture, improving sentiment is being reflected in capital recycling activity, including the December repayment of a NZD$24m maturing retail CRE loan and the sale of a major land parcel at Mangawhai Central to an institutional counterparty.

Portfolio positioning continues to reflect our core macro view that fiat currency risk remains structurally elevated into 2026, reinforcing the role of senior secured lending against hard assets as a portfolio hedge. With inflation more persistent in Australia and diverging from New Zealand’s easing cycle, maturing loans are being actively rotated, including the recycling of the York Street Sydney office asset (now under contract).

New Zealand’s easing cycle is now translating into improving economic momentum. Business surveys point to stronger trading conditions, hiring and capital investment expectations through 2026, while manufacturing activity has accelerated to its fastest pace in four years. Net migration has also stabilised following the 2024–25 downturn, supporting household formation, housing demand and construction sector capacity.

Looking ahead, portfolio positioning remains focused on disciplined capital rotation rather than volume-driven deployment. As refinancing activity, asset sales and staged development settlements increase, capital will continue to be recycled into opportunities with multiple repayment pathways, strong sponsor execution capability and demonstrable end-market demand.