March 20, 2026

Real Asset-Backed Private Credit: Liquidity and the Nature of Lending

Share

Markets periodically remind investors of the difference between liquidity and the expectation of liquidity. Recent headlines, including elevated redemption requests and withdrawal limits at several large US vehicles, highlight a mismatch between fund structures and the underlying assets, rather than a deterioration in asset quality.

It is important not to let liquidity mechanics obscure the fundamentals. Real Asset-backed private credit remains a defensive investment that plays an enduring role in financing the real economy. Investors have historically been well compensated for providing this capital, and structural demand for private lenders remains strong. Over the last decade, we have financed more than $10bn of real assets across commercial real estate, farmland agriculture, infrastructure and resources, from which several consistent lessons have emerged:

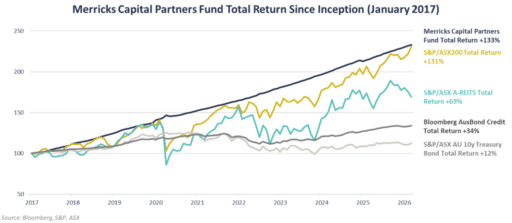

- The risk of capital loss in senior secured, asset-backed lending is low when projects are taken through to completion. Even where delivery is delayed or requires additional capital, underlying asset value and lender security rights provide strong recovery pathways. Since 2017, impairment has been <0.3% p.a. while delivering net ~10% annualised returns (>130% total return), comparing favourably to other income-oriented asset classes (A-REITs 69%, investment-grade credit 34%, government bonds 12% total return since 2017; sources: Bloomberg, S&P, ASX).

- These returns have been delivered with relatively low volatility across cycles, including periods of asset valuation declines (office during 2022 cap rate expansion) and externalities impacting agriculture (floods, bird flu, export tariffs). While income and capital growth are treated differently for investors, outcomes have been comparable to an equity risk premium. Importantly, we have consistently managed 5–15% of the portfolio in non-performing loans while delivering commercial outcomes, highlighting both the defensive nature of the strategy and the need for aligned liquidity.

- As we’ve noted for a number of years now (see our Year Ahead 2025), these equity-like returns reflect both credit risk and a liquidity premium earned for lending against less liquid, asset-backed investments. Liquidity is the trade-off investors accept, which we estimate contributes between 2–3% of returns depending on the cycle.

- Delivering true alpha in private credit sits at the platform, portfolio and investment level. Experienced teams, strong origination networks and active portfolio management allow capital to be allocated across uncorrelated real asset sectors, creating diversified income streams that are less reliant on any single market cycle.

- It is clear the retail market is coming to appreciate that private credit spans a spectrum of liquidity profiles, from illiquid, asset-backed lending through to more tradable credit. What we are seeing in current institutional allocations is a clear understanding of this trade-off, with capital continuing to flow toward strategies where liquidity terms are aligned with underlying asset duration.

Periods like the current one can also create attractive conditions for new lending. When capital becomes more cautious, and some lenders retrench, pricing discipline improves, structures tighten, and borrowers place greater value on reliable funding partners. Historically, these environments have produced some of the strongest vintages for private credit, as lenders are able to deploy capital into transactions with wider spreads, stronger covenants and improved downside protection. The current headlines serve less as a warning about private credit and more as a reminder of the nature of the asset class itself: attractive long-term returns are rarely achieved without accepting some degree of illiquidity along the way.