May 1, 2026

Agriculture’s Inflation Link: Higher Prices, Slower Supply

Share

Agricultural markets are in a period where higher prices are not producing the supply response markets might normally expect. Logistics, labour, water and input constraints are limiting the production response to higher commodity prices. Drawing on two decades of providing capital to agriculture across Australia and New Zealand, several themes are clear:

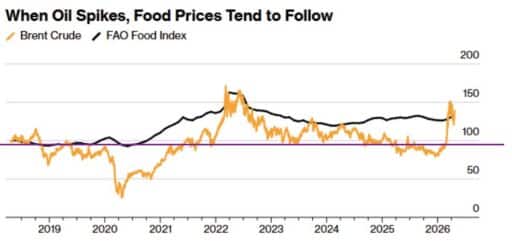

- Food inflation typically lags energy inflation. Rising oil prices first affect fertiliser, fuel and logistics before feeding into planting decisions and crop yields. Across major production systems, fertiliser and fuel costs typically account for approximately 30–50% of grain production costs, 10–20% in horticulture and 5–15% in grazing systems (based on borrower reporting).

- Fertiliser markets remain the primary transmission channel. Nitrogen fertilisers underpin approximately 50% of global crop production, with natural gas accounting for up to 70–80% of nitrogen fertiliser production costs (IEEFA), meaning disruptions in energy markets can influence crop yields across multiple growing seasons.

- Water availability risks are increasing. Murray–Darling Basin storages are estimated to be ~20% below long-term averages (Kilter Water), with below-average inflows and an increasing probability of El Niño conditions into late 2026. In the United States, historically low Western snowpack levels also point to reduced irrigation availability ahead of the Northern Hemisphere growing season (USDA).

- Traditional bank models are less flexible when operating margins tighten. Higher input costs and seasonal volatility can reduce serviceability headroom, increasing demand for structured capital secured against productive land and water assets.

- Portfolio construction remains key to managing the risks that arise from geopolitical and agricultural seasonality. Our farmland agriculture credit strategy is diversified across 25+ senior secured loans further diversified by commodity and growing regions in Australia and New Zealand. Since inception, the strategy has generated annualised investor returns of approximately 10%.

Note: Data is normalised with factor 100.

Source: ICE Future’s Europe, UN’s FAO.

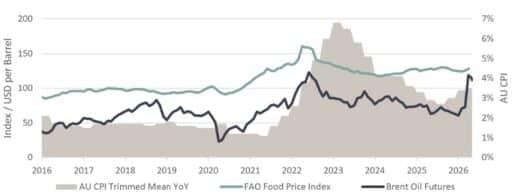

Source: ICE UN ABS.

Fundamentally, periods of rising input costs can pressure working capital requirements in the short term, but agricultural producers have historically benefited from higher commodity prices and farmland values that tend to appreciate with inflation. For lenders, this creates a constructive environment: borrowers need capital to manage volatility, while loans secured against productive land and water assets remain supported by essential demand, inflation-linked collateral and improving deployment opportunities.