July 22, 2022

Impact of Rising Rates on Real Estate Valuations

Share

- Our base case macro assumption is that Australian 10-year bond yields have normalised back to a pre-covid level of 3% – 4% p.a.

- This may result in real estate valuations coming under pressure over the next six months as transaction data is accumulated by valuers.

- Rising inflation and flow through to higher rentals may cushion the overall impact but we will manage our portfolio on the basis that valuations could decline by 10% – 15%.

- With a combination of modest loan to value points and a book of CDS insurance investors will be protected whilst benefiting from the rising base rates in our portfolio.

- Below we examine the resiliency of office valuations in this paradigm, compared to agriculture, residential, hotels and infrastructure this sub-sector has a wider array of potential demand outcomes.

An eye on commercial office yields

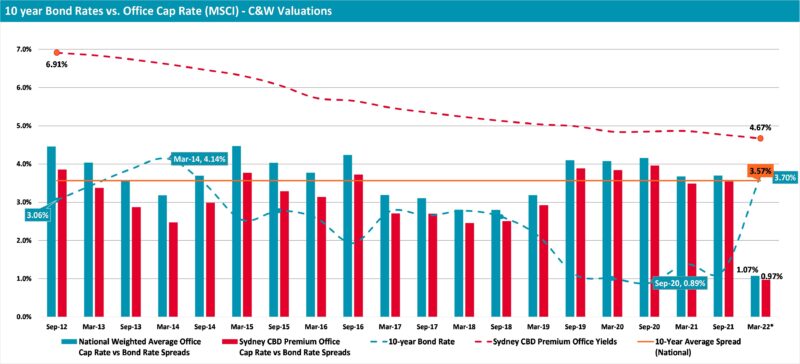

When assessing investment opportunities in the office sector we analyse the spread between commercial office capitalisation rates (cap rates or yields) and 10-year bond rates. Currently the spread between prime office cap rates and the government bond rate is just over 1%, significantly below the long-term average of around 3%.

As the Reserve Bank of Australia ‘normalises’ interest rates as expected, we will see pressure for cap rates to rise as debt costs become higher.

A key valuation methodology for income producing assets like office buildings is cap rates or rental yields. As transaction data is accumulated over the next six months, unless rents increase proportionally, it is possible we will see asset values soften due to cap rates going higher.

With rising inflation and building replacement costs we expect rental in premium office buildings to rise and to some degree offset any cap rate expansion (lower valuations). The extent to which office rental increases is more uncertain when contrast to rental/income in other subsectors of our portfolio of loans, as vacancies are higher and the normalised level of office demand is still uncertain.

Reference: Cushman & Wakefield Valuations

Over the past twelve months, we have decreased our exposure to commercial office projects based on our view that interest rates were likely to rise quicker than central bank guidance (accordingly, we have reduced our office sub-sector allocation from 26% – 18% as of 30 June 2022 for the Merricks Capital Partners Fund). The loan to value attachment point of office loans was also reduced from 65% – 70% to 55% – 65% on new loans written.

We don’t see a correction of cap rates or potentially softening valuations as inhibiting the strategic allocation of capital to new loans backed by high-grade assets but rather, we are managing these investments with the expectation that underlying office values could decline.

There is significant demand for capital within the office sub-sector, creating the opportunity for Merricks Capital to be highly selective with respect to the investment metrics outlined above. We have >$750m of prime office commercial real estate investments in due diligence that meet our target returns, satisfy valuation sensitivity analysis and possess compelling investment fundamentals that we intend to reach financial close on in the second half of 2022.