Merricks Capital provides innovative investment solutions that deliver consistent performance for its investors while operating with financial discipline and prudent risk.

Our investment strategies include private credit across commercial real estate, agriculture and infrastructure and specialised industrial.

Established in 2007, Merricks Capital delivers a truly differentiated multi-strategy offering, with extensive investment capability and global experience spanning multiple asset classes.

Disinflation tailwind and tight spreads – implications for senior real-estate credit

Share

Shifts in global disinflation and local monetary policy are creating a more supportive backdrop for Australian real estate credit. At the same time, investors face late-cycle conditions with tight spreads, making disciplined portfolio positioning critical.

Key observations

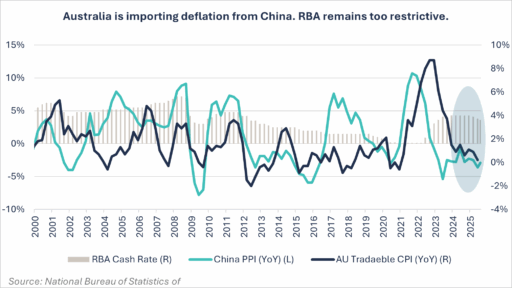

China’s ongoing producer-price deflation is exporting disinflation into Australia via tradables and input costs, while domestic labour markets soften.

We expect this could result in an RBA policy shift from restrictive toward neutral, making a cash rate with a “2-handle” plausible over the easing cycle.

Lower cash rates will anchor bond yields and cap rates, improve asset valuation certainty and support debt-serviceability, widening refinance pathways and underpinning secured lending strategies.

We’re seeing construction input costs plateauing with builders and developers commenting on imported materials being cheaper and signs softening local labour conditions are tempering wage and subcontractor rates, albeit region specific.

Credit spreads are compressed to late-cycle levels, which we are using to our advantage by buying CDS protection at lower cost. This provides cheaper portfolio insurance and reinforces resilience against left-tail macro shocks.

Stronger bid depth in real estate is supporting refinancing for new borrowers and enabling exit opportunities for existing borrowers, while private credit continues to capture equity-like returns through structural premia such as liquidity, complexity and covenant protections.

We see development pipelines emerging or re-opening across build-to-rent, student accommodation and mixed-use projects, with over $1bn of pipeline opportunities progressing across our funds. In this late-cycle environment of tight spreads, our focus is on preserving yield through structural premia while retaining flexibility to reprice risk. The portfolio remains short-dated (~11 months average maturity) and is supported by low carry and convex hedges that are inexpensive to maintain at current spread levels. This deliberate positioning allows us to capture income from new opportunities while protecting the portfolio against potential macro shocks.