November 2, 2025

Fed’s Balance Sheet Pivot: Implications for Real Estate and Credit Markets

Share

- This week we have had clear direction from the Reserve Bank of Australia (RBA) and the Federal Reserve (Fed) in the USA that further rate cuts in November are unlikely.

- Whilst our base view is that the overnight interest rates are going lower next year, these short-term rates may be less important in driving the underlying transaction volume in real estate and infrastructure.

- Liquidity in the global 5-yr and 10-yr bond markets will be a key determinant in setting the risk-free benchmark which all assets are priced.

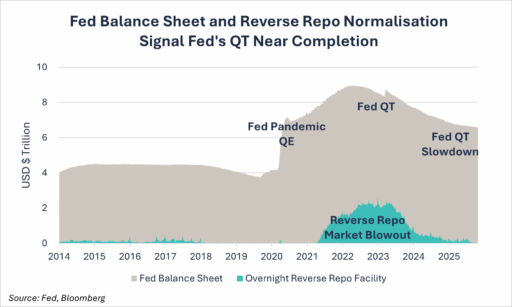

- The announcement of the Fed ending of Quantitative Tightening (QT) this week is pivotal as it reinjects $40-50bn of buying back into bond and mortgage markets.

- If the “800lb gorilla” is now driving bond markets in a different direction we think there is far less risk that bond yields go higher.

- The confidence in a stable rate environment moves the risk framework for long duration yield investments such as real estate.

- In our view, rates now stay flat or go lower if there is some economic shock, but the risk of going higher has been reduced.

The Fed has hit a clear liquidity inflection after two years of balance sheet contraction. Since April 2022, assets are down about US$2.4T to ~US$6.6T and the Overnight Reverse Repo Facility has fallen from US$2.4T to ~US$10B, signalling scarce excess cash. The Fed will end QT on 1 December 2025, reinvesting Treasuries and redirecting agency mortgage-backed securities into Treasuries, alongside the October 25bp cut to 3.75–4.00%. That puts US$40–50B/month of price-insensitive demand back into the market, anchoring the long end and reducing upside yield risk as reserves stabilise.

In Australia, a hotter CPI delays RBA cuts, but our medium-term view stays disinflationary, helped by China’s PPI deflation and softer domestic demand. Capped global yields plus a cautious RBA improve underwriting visibility: lower-volatility term rates and deeper bond liquidity support valuations, refinancing and deal flow. This is a constructive setting for senior, asset-backed private credit. Better liquidity and a capped risk-free rate improve exits without loosening covenants. We’ve already seen ~A$575m of repayments and ~A$840m of deployments YTD and expect ~A$700m of further repayments and ~A$1.5bn of new funding over 12 months as conditions ease into 2026.