October 3, 2025

Diversifying Portfolios with Uncorrelated Gold Exposure

Share

Private credit is at its strongest when it finances a set of uncorrelated hard assets with multiple pathways to repayment. For several years, we have been looking to add gold sector exposure to the fund as a diversifier and inflation hedge.

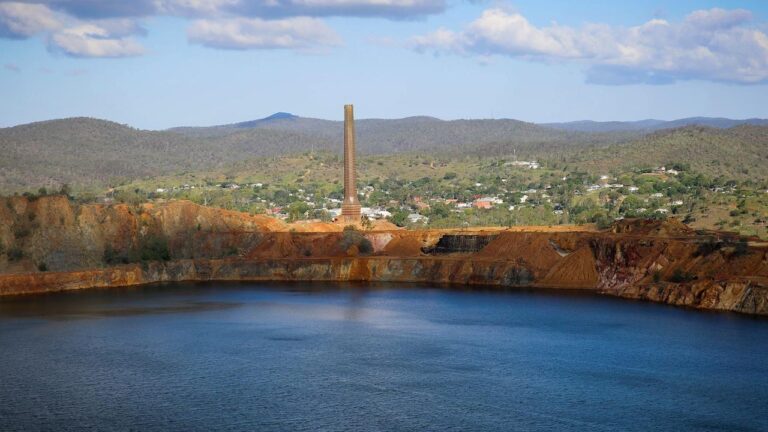

The $132m loan for the recommissioning of Queensland’s historic Mount Morgan gold mine, delivered in partnership with the Northern Australia Infrastructure Facility (NAIF) and sponsor Heritage Minerals, illustrates this approach. The project converts an environmental liability into a defensive credit underpinned by government support, proven technology and favourable commodity economics.

A few key considerations from a transaction we began due diligence on in 2022:

- Our 24-month process to close on the Mount Morgan finance agreement included independent consultant reviews of resource quality, tailings facility design, processing flowsheet and CAPEX contingencies. The project uses conventional processing supported by innovative cost saving cyanide reprocessing technology that is now well tested around the world.

- Environmental liabilities are often underestimated. Tailings projects frequently carry legacy risks that complicate permitting and water management. Here, the Queensland Government’s $17m underwrite towards rehabilitation and indemnification against many of the future environment liabilities provides a rare public sector backstop, materially strengthening downside protection.

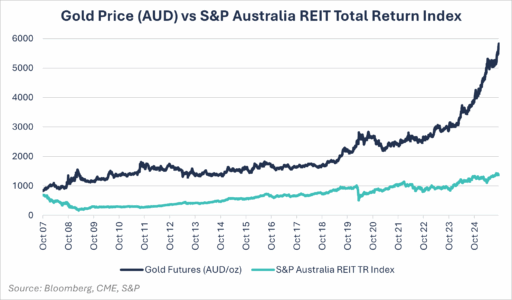

- With an all-in sustaining cost of AUD$2,350 per ounce, Heritage sits towards the lower end of the Australian cost curve providing significant downside protection to any gold price movements. At a current spot gold price of AUD$5,800 per ounce, the Mount Morgan mine has a margin profile that supports more than 2.5 times debt service coverage and will see an accelerated repayment profile should the gold price remain high. With a minimum earn in place the facility will generate the same quantum of interest, but in a much shorter time frame. This call protection is expected to provide significant upside to the gold price.

- More than $100m of CAPEX and sponsor equity has already been contributed, creating resilience against cost overruns and a project that is nearing commissioning.

- Bringing together double-digit investment returns and environmental impact continue to be rare, however as a significant non-financial benefit this loan will help facilitate the clean-up of the 100yr old mine site which has been leaching sulfuric acid and other toxins in water ways and Great Barrier Reef.

For the Merricks Capital Partners Fund, Heritage Minerals will be a 3-4% allocation in an increasing diversified portfolio, as infrastructure and agriculture are also growing in portfolio weighting. The exposure complements the Fund’s defensive positioning by providing access to a globally sought after commodity with multiple risk mitigants. With deep domain experts across Regal Partners our ability to source underbanked real asset sectors, apply deep technical and financial diligence, and structure loans that minimise the risk of principal loss while capturing equity-like returns is ever expanding.

More broadly, we see three themes continuing to define the opportunity in private credit:

- Sustained population growth in Australia and New Zealand is driving long term demand for housing and infrastructure.

- Global food demand, coupled with the export strength of Australia and New Zealand, is underpinning agricultural credit opportunities.

- With equity markets trading at full valuations, we expect scenarios where real assets outperform in 2026, offering investors downside protection through expanded refinance opportunities for our borrowers.

Across these themes, private credit remains distinctive and defensive: investors are compensated not by leverage or subordinated positions in the capital stack, but through the structural liquidity premium embedded in bilateral senior secured loans.