Merricks Capital provides innovative investment solutions that deliver consistent performance for its investors while operating with financial discipline and prudent risk.

Our investment strategies include private credit across commercial real estate, agriculture and infrastructure and specialised industrial.

Established in 2007, Merricks Capital delivers a truly differentiated multi-strategy offering, with extensive investment capability and global experience spanning multiple asset classes.

Fewer Starts, Stronger Finishes: Construction Credit Outlook 2026

Share

In recent weeks our team has met with dozens of property and infrastructure developers and builders in Adelaide, Brisbane, Melbourne, Perth and Sydney. The key message is that Australia’s construction cycle is transitioning into a new phase where rampant inflation and capacity shortages (outside Brisbane) are well behind us, with new work slows and Chinese material supply now abundant. The forward pipeline has softened, with fewer new project starts flagged for 2026. At the same time, we are seeing fewer open market tenders, with developers increasingly favouring Early Contractor Involvement procurement models that prioritise delivery certainty over competitive tendering.

For market participants in equity and credit, the forward cycle most likely carries less delivery risk, and the potential investment outcomes will be determined by the traditional drivers of economic rent and cost of capital (interest rates). The majority of investments that finance existing real property will also be less at risk from new supply.

Public infrastructure is generally slowing into 2026 outside Queensland, with NSW and VIC largely focused on completing existing megaprojects. Infrastructure Australia now estimates the five-year pipeline at $213b, down 8% on 2023, with transport past peak and a pivot toward energy and social projects.

Private sponsors are also deferring or shelving projects at the pace set during 2020–23, leaving the forward pipeline shallower. July approvals show the trend clearly: total down 8.2% month-on-month, apartments off 22.3% and detached houses up just 1.1% (ABS).

Market signals in the crane index reinforce this rotation. Residential, mixed-use and data centres are the few growth areas (+6 cranes for data centres to 32), while commercial (–24) and civic (–12) activity is contracting, underscoring the sectoral shift underway. (RLB Crane Index – Q3, 2025).

Melbourne continues to have the most grim forward outlook in discussions with builders and this will further reduce the current crane count down 37% compared to 2019, when Government Civil work and Data Centres are excluded. Ironically this makes the few projects progressing in this jurisdiction lower risk.

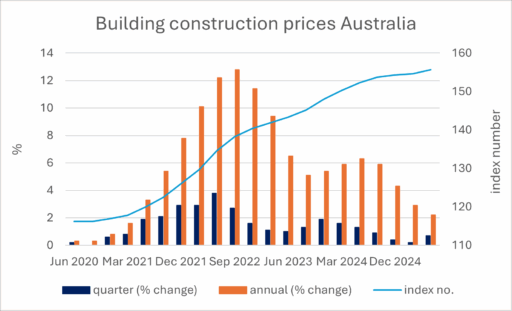

Materials inflation has plateaued after several years of volatility, reflecting both softer global demand and the impact of supply normalisation. China’s domestic slowdown and US tariffs is pushing excess capacity into export markets, reducing price pressure on key inputs like steel and fabricated products.

From 2024 onward, funded projects in our portfolio have generally delivered on or ahead of program. Recent examples include Victoria Tower Adelaide, a 38-story residential build-to-sell project, which reached practical completion 11 weeks early, and the Kimberley Marine Support Base or Broome floating port project, which was delivered on time despite its complexity and is now operational.

Source: Australian Bureau of Statistics, Producer Price Indexes, Australia June 2025

For private credit investors, the cycle shift from scarcity to potentially spare capacity changes the risk equation. With fewer new starts, contractors are competing harder for funded projects, while a stabilising cost base is making outcomes more predictable. This gives lenders greater confidence in construction completion against fixed-price contracts, cleaner refinancing pathways and timely capital recycling. The key variable that could change the market is equity re-entering, as feasibilities are reworked under a lower interest rate environment, which would activate a new wave of project starts. Regardless of that timing, we believe that construction funding currently offers more predictable delivery and returns in 2026.