Merricks Capital provides innovative investment solutions that deliver consistent performance for its investors while operating with financial discipline and prudent risk.

Our investment strategies include private credit across commercial real estate, agriculture and infrastructure and specialised industrial.

Established in 2007, Merricks Capital delivers a truly differentiated multi-strategy offering, with extensive investment capability and global experience spanning multiple asset classes.

Merricks Capital increasing credit hedging on the back of a market rally

Share

In our view, Government bond yields (and central bank cash rates) may be reaching their peak. However, high sovereign debt levels and fiscal budget deficits combined with inflationary pressure have reduced the government’s capability for major intervention in future years.

Investors need to resume the responsibility of managing and hedging the credit risk in their portfolios. The market stability over the last 15 years has been overly reliant on government stimulus and rescue packages as credit protection.

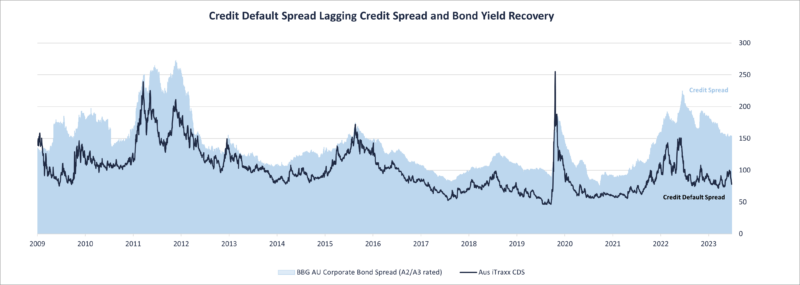

The good news for hedgers is that the cost of hedging has not yet increased despite the structural shift away from potential bailouts. This is surprising, given the stress starting to appear in the economy.

Despite the RBA cash interest rate increasing by 4% since March 2022, Credit default spreads (CDS) have remained tight (black line in the chart below). Credit default spreads on Australian sovereign, Australian banks and Australian investment grade corporate bonds stand out as the hedging instruments for the Merricks Capital Partners Fund (the Fund) to mitigate this tail risk due to its low premium cost and higher convexity in payoff.

We’re not forecasting a major credit crisis from our borrowers. However we identify one of the systematic refinance risks in Australian and New Zealand hard asset lending is a significant widening in the cost of debt over the reserve bank rates.

A likely higher-for-longer rate environment has also resulted in an 80% decline in commercial real estate transactions in Australia in 2023. Less liquidity in the sales market combined with refinance risk looming in credit markets suggests we are being prudent maintaining

In addition to the loan to valuation (LVR) buffer (Partners Fund average LVR 61%), credit insurance is important to protect the portfolio during the price discovery phase the real estate sector will likely enter in 2024-25.

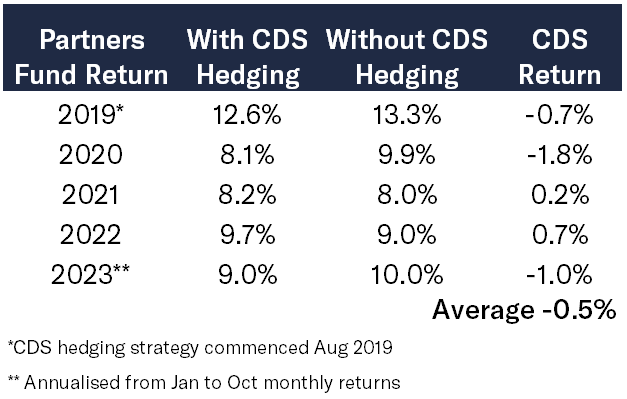

Over the years, the tight credit default market has allowed the Partners Fund to hedge credit risk at an inexpensive cost relative to the macro uncertainties in the market. The cost of CDS hedging for the fund averages at approximately 50-60bps per annum, as illustrated in the table and chart below.

Equity and bonds have rallied aggressively this month on the back of the US Federal Reserve pause and weaker-than-expected US CPI data. This has trimmed back credit default spreads further, resulting in lower mark to market for CDS positions in the Fund. We see the pullback in spreads as an opportunity for the Fund to increase credit protection as the Fund grows.