May 5, 2023

Why fixed rate loans play an important role in a defensive private credit portfolio

Share

We recently settled a $31m residual stock facility in a fast-growing suburb of Melbourne. What was unique about this loan was that it was the first time in almost 18 months we’d used fixed-rate pricing for a commercial real estate investment.

Since February 2021, we’ve been moving our portfolio to floating-rate loans in anticipation of an accelerated cash rate hiking cycle. Currently, more than 65% of our senior secured first mortgage investments are floating in the Merricks Capital Partners Fund.

While only using floating rate loans can sound attractive during rate hike cycles, this can potentially overlook the risk associated with pricing a variable loan when interest rates are volatile and closer to peak (2-year AU bond yield is currently 3.1%, after climbing to 3.6% in February and falling to 2.9% in March 2023—Bloomberg).

The Reserve Bank of Australia’s (RBA) latest 25bps hike surprised the market and reminded participants that the interest rate trajectory remains unpredictable. While some aspects of inflation are cooling, our discussions with developers and builders indicate that certain inflation drivers, such as the cost of labour and rent, are expected to remain elevated throughout 2023 and continue into 2024.

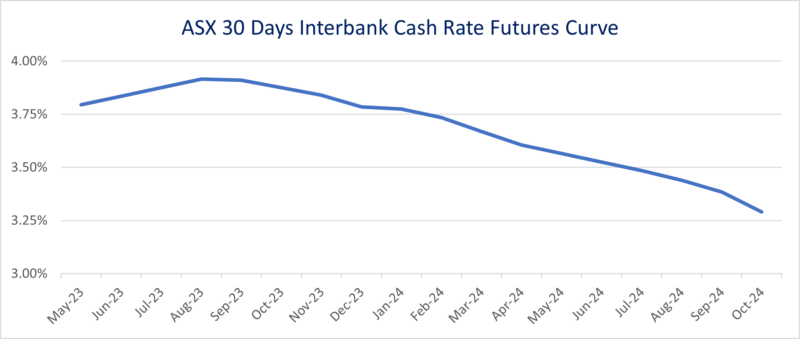

The current AU yield curve, shown in the chart below, implies that today’s RBA rate may only be 3-4 months away from the peak of the cycle, and backwardation of the yield curve from Q3 this year has reintroduced potential downside risk to reference rates and variable loans.

We could probably make the case for higher rates in the future, but 30 years of market experience cautions us against attempting to predict the forward rate curve when there’s an option to lock in attractive fixed rate pricing on short duration loans.

Source: ASX

In our experience, we often attract higher-quality investments and borrowers with a fixed-rate loan offering where fixed rates provide these borrowers with additional certainty on project costs, for which they’re usually willing to pay a premium.

Fundamentally, we believe that a 10% net return to investors for senior loans on real estate assets that are likely generating 5-6% yield and geared at <65% LVR is a highly defensive strategy within our portfolio construction.