August 5, 2022

What is on Investors’ minds?

Share

This week’s market insight expands on three topics at the forefront of Investors’ minds.

How sensitive are portfolios to inflationary pressures and what changes have been made in response to rising inflation and interest rates?

In short, inflation is leading to higher rates and lower valuations of underlying loan collateral. This has led to our focus on reducing loan to value ratios (LVRs) across portfolios.

In response to the continued risk of inflationary pressures, we have implemented the following changes over the past year:

- The use of floating rate loans: since mid-2021, we have predominantly used floating rates for new loans in the portfolio. Today, a 100 basis point increase in the RBA cash rate lifts underlying loan income performance by an estimated 55 basis points per annum. In September 2022, this correlation is forecast to rise to 70 basis points of additional loan income for a 100 basis point cash rate rise.

- Increased portfolio diversification across 14 asset subsectors: we estimate this should reduce market risk and borrower concentration risk.

- Reduced portfolio LVR: we consider it probable that rising interest rates and reduced credit availability could see some real estate prices pull back an estimated 10-15% from recent peaks. This will impact some borrower equity but should not impair our senior debt position due to a significant borrower equity buffer. The Merricks Capital Partners Fund has seen the average weighted LVR reduced from 65% to 62% over the past 12 months, providing further equity buffer.

What is your opinion on lending to construction projects and the perceived increased risk?

In 2021, we significantly reduced our exposure to construction loans as there appeared to be irrational lender pricing and builder bidding to win projects at zero margin.

Today, our portfolios do not have exposure to any projects where builders are known to be in financial distress. We have doubled down on due diligence and review of this risk over the past 12 months. There is heightened awareness in the industry around insolvency. Escalating building costs have already seen additional contingency added to most build contracts and project feasibilities.

Competition to fund development projects has now reduced, allowing for stronger covenants and higher potential senior debt returns.

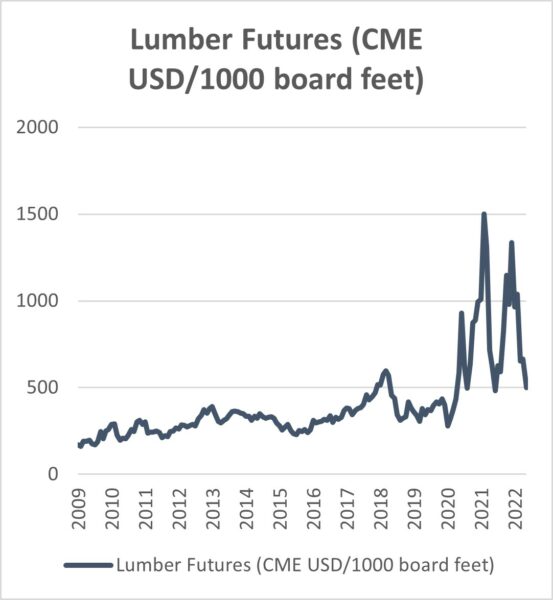

Whilst labour costs are expected to continue to escalate, other key input costs are showing prices have fallen significantly from the short squeeze experience in many markets at the beginning of the year. They show that Lumbar and Rebar prices have normalised over the past 6-8 weeks from Q1 2022 highs.

Stronger covenants, receding material prices and wider interest rate margins lead us to believe it is sensible to again pursue select loans in development funding.

What is the impact of using Credit Default Swaps (CDS) and do you actively trade your hedge portfolio?

The Merricks Capital Partners Fund runs a ‘macro credit hedge’ across the portfolio using a basket of CDS positions. This basket consists of Australian sovereign CDS, Australian banks CDS and iTraxx CDS to hedge against declining general credit market conditions and are held to create liquidity for the Fund in times of adverse market volatility.

This insurance in the Merricks Capital Partners Fund provides additional risk management whilst we continue to lend money prudently in these uncertain times. Based on historical credit events, this hedge could potentially add 10-15% to portfolio returns in the most extreme macro environments.

The cost of employing this hedge is roughly 50 – 70 basis points which we consider to be attractive relative to the 1000 basis points we are receiving for making private loans.

With heightened market volatility, this hedging strategy has been performance additive this year as credit spreads have widened with increasing risk aversion.

We have no intention of trying to time markets by trading in and out of our insurance book as it is there for protection against extreme events.