February 3, 2023

Migration upside creating an investment opportunity

Share

- An impending influx of international students is expected to put pressure on rental vacancy rates over the next two years. Forecast higher rental yield growth in inner city locations provides upside for residual apartment stock and residential construction projects despite further expected declines in residential property values.

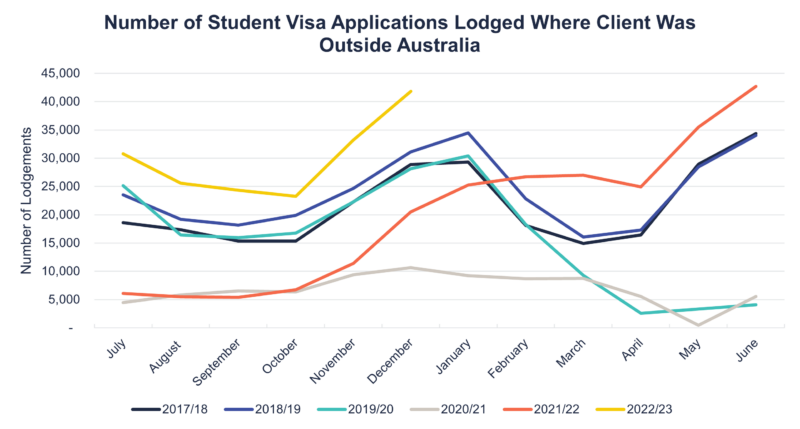

- Annual population growth, driven by returning net overseas migration (NOM), recovered in 2022 to June 2020 levels (1.1%) and nearing pre-pandemic growth levels of 1.5% (June 2019). The Centre for Population has forecast NOM to return to the long-term pre-pandemic average (235,000 people) in 2023, but there is a potential upside to this forecast based on December NOM figures by ABS and the applications of student visas from the Department of Home Affairs.

- Applications for student visas serve as an indicator of future student numbers. Above average visa lodgements from February 2022 to December 2022 (see graph) suggest above average student inflows in 2023 which will likely flow through to 2024 and 2025 as students complete their education.

- We expect demand for in-person classes to continue to be above average pre-pandemic levels across 2023 and 2024. This is further buoyed by expected higher demand from students from India (Australia’s second largest consumer of international education) following the implementation of the Australia-India trade deal late last year, allowing Indian graduates of Australian institutions to remain in Australia for up to four years.

- Residential asset values decreased by 7.2% in 2022 with a further potential fall of 15% possible in the current interest rate cycle.

- An area of opportunity arising from the residential market dislocation is ‘residual stock facilities’ or newly completed apartments. We see stronger resilience in new apartments relative to other sectors of private credit in a higher interest rate environment, as tight demand (~1% vacancy) and increasing rental yields underpins how far valuations will come off. According to SQM Research, rental yields for units in Sydney and Melbourne increased by 17.1% and 13.9% respectively during 2022 and yields continued to increase in January 2023 (4.9% and 2.4%).

- The Merricks Capital Partners Fund currently has a 10% exposure to residential real estate assets and 6% to residual stock facilities.

Source: Department of Home Affairs (2023)