April 5, 2024

Liquidity returning to the Land of the Long White Cloud

Share

- This week, the Merricks Capital Partners Fund’s (the Fund) single largest borrower (8.5% of NAV) has contracted for more than $80m of unconditional asset sales. This asset sale of a town centre and residential development project 80km north of Auckland is expected to reduce the effective LVR to under 40% by July 2024.

- This is one of several key outcomes achieved with our New Zealand (NZ) borrowers this year, including contracted property sales for a Hawkes Bay apple orchard business and commercial leases at 15-20% above 2023 valuations for an Auckland CBD office refurbishment project.

- Over the past two years, we have increased the Fund’s NZ exposure from 16% to 35%. This is consistent with our view that a higher rate environment and a less crowded lending market would drive highly favourable senior debt opportunities.

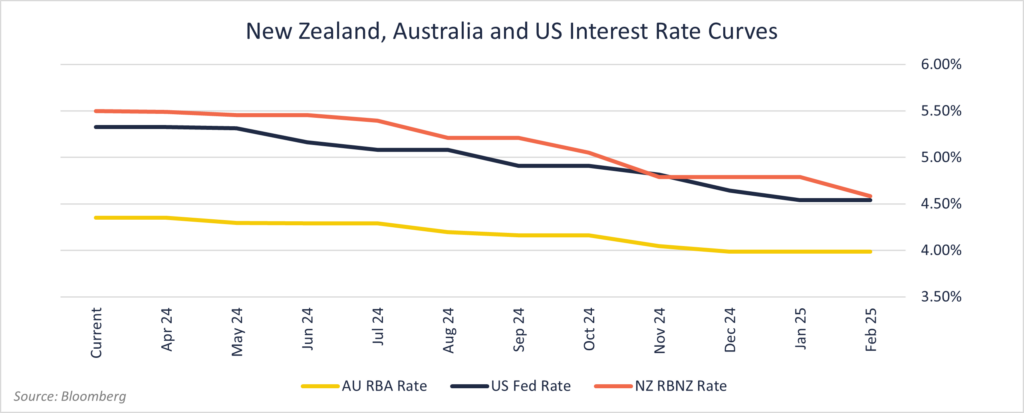

- NZ 10-year bond yields have consolidated at an 85bps discount to today’s 5.5% rates, with NZ’s interest rate implied to fall by 90bps in the next 12 months. With markets forecasting forward rates to normalise, we anticipate a continued uptick in NZ real estate transactions.

- The expected refinance of overweight exposures in New Zealand and office markets in the coming months gives the Fund the opportunity to reweight into several key macro themes, particularly residential (apartment buildings) and agriculture. Loans currently in due diligence provide a significant opportunity to increase our residential asset allocation over the next quarter (currently 11% of the Fund and 40% lower than 3-5 years ago). With structural tailwinds of undersupply and high migration in Australia and New Zealand underpinning low vacancy and strong rental growth, the credit quality of this sector continues to improve.